Are you relying too much on your provident fund (PF) and

Public Provident Fund (PPF) investments for your own good?

Your confidence maybe misplaced. Here’s why.

The PF savings myth If a 35-year-old person earning a

monthly basic salary of Rs.25,000 saves uninterrupted for the next 25 years,

with wages increasing every year by 10%, he would save only Rs. 24.35 lakh*.

Since many employers deduct 12% of the entire basic amount, even then he would

end up with Rs 1.58 crore* of retirement corpus and a monthly pension of Rs

5,375 against the requirement of a corpus of Rs. 3.67* crore to last for 20

years into retirement. This is assuming a monthly expense of Rs.30,000 and

annual inflation of 7%*. In short, the person will end up with a shortfall

ofRs.1.09 crore.

These numbers have to be seen in the background that very

few people make uninterrupted contribution to EPF, or PPF for that matter, till

their retirement. A majority of people make premature withdrawals during

home-buying, medical emergencies, child’s higher education and wedding and, so

on. This means the shortfall is our case is likely to be even more. Clearly,

relying only on EPF savings is insufficient to lead a care-free life in the

future.

Section 80C limits constrain PPF savings:

Theoretically, you can annually invest uptoRs. 1.5 lakh in

PPF. But most people don’t since there are other items that also qualify for

this deduction, be it home loan principal repayment or child’s tuition fee.

Even when you can save a higher amount, you might be tempted to not do so

beyond the available Section 80C amount, like most people.

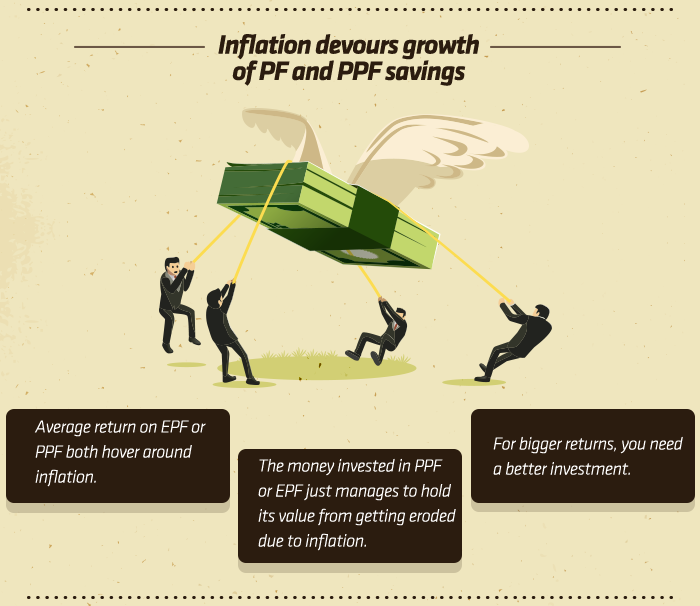

How inflation devours growth of PF and PPF savings:

Since 2005-06, the annual return of EPF has been ranging

between 8.25% and 9.5%, while annual interest rate offered on PPF has ranged

between 8% and 9.5% during the same period. Elsewhere, the average annual

retail inflation during 10 years period till December 2014 was 8.35%**.

However, since you need a substantial amount to fund your

different future needs and help you lead a carefree life, you need an

investment where your money’s growth runs far ahead of inflation. This is where

investment in equities comes to the picture.

Enter equities investing through ULIPs:

*Business Standard, November 23, 2014, ** Average of annual

CPI number reported by World Bank.

Hi,I am Ritika Shah working with insurance comapny as insurance adviser owing good knowledge of various policies such as ULIP Plan Comparison, ULIP Insurance India, Best ULIP Insurance Policy,Best ULIP Insurance Plan, ULIP NAV,ULIP Ulip Plan ComparisonUlip Plan Comparison,Best Ulip Insurance plan

ReplyDelete