Tuesday 31 May 2016

Wednesday 25 May 2016

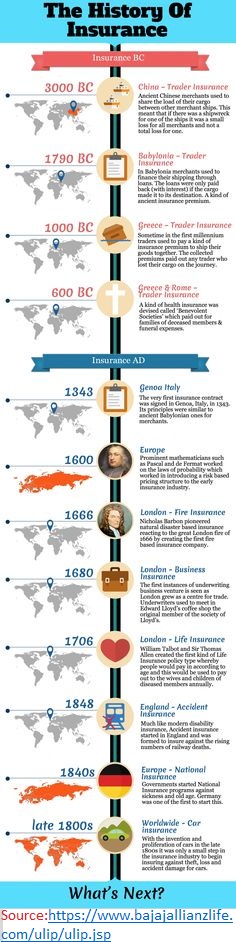

ULIP-Insurance

ULIP

plans offer the flexibility of market linked returns on your investments and

life insurance cover for you and your family. For more details: https://www.bajajallianzlife.com/ulip/ulip.jsp

Monday 16 May 2016

Why you should avoid the ULIP trap

This blog has seen its fair share of ULIP Products in the

past and I have always been against ULIPs that charge exorbitant fees &

charges from their investors as well as agents selling ULIPS just to make a

fast buck. Unfortunately not many investors know about ULIPs and their fees

& charges and have fell into the trap. The idea behind this article is to

bring to your notice some shocking news I read in the new today as well as some

suggestions for you if you are a prospective or current ULIP Investor.

ULIPs are

not investment products

Agents & Sellers of ULIP Products rarely mentioned the

fact that ULIP Products are primarily Insurance products. Instead they sold

them as investment products. Each of these agents had one fancy work-up

calculation that would hypothetically predict a 20% or 30% returns year-on-year

and say that if you Invest Rs. 2 lakhs per year for 10 years you will get

something like 2 crores at the end of 15 years.

ULIP

Returns are linked to the Stock Market Performance

Agents & Sellers will never mention the fact that ULIPs

aren't invincible. They will never tell you that your ULIP can make losses in

case the market tanks. They keep lay the honey-trap so well that as an

investor, you fail to realize that ULIPs can make losses and end up investing

in schemes that are highly aggressive and invest almost the entire corpus in

Stocks.

ULIPs

aren’t the only tax saving instruments

One of the biggest selling points for Agents is the tax

benefit for Investors. There are numerous other tax saving products and many of

them are 100% safe and don’t have the kind of risks that ULIPs have. So, don’t

get fooled if your agent is trying to convince you that these are the best tax

saving options. Unfortunately they are not. There have been many articles about

tax saving in this blog.

he Fees & Charges are not explained clearly to Investors

When the Agent is selling his ULIP Product to you, he will

not mention the fees & charges the Insurance Company that is providing this

Ulip Plan

Comparison is going to deduct from your annual premium ever year. This

is because these charges form a significant chunk of the premium you pay every

year. So, realistically speaking around 10% and as much as 40% of your premium

goes to the agent & his company just for selling this product to you.

Even in the mathematical work-up they show you, they will not

consider this chunk that goes into their pocket and their calculation will

always show that 100% of your investment is considered as an investment.

Source: http://bestulipinsurancepolicy.tumblr.com/post/144449362614/why-you-should-avoid-the-ulip-trap

Tuesday 10 May 2016

SHOULD YOU STICK TO YOUR ULIP OR SURRENDER IT?

Most investors in ULIPs have battled with this issue at one

time or the other. In most situations, the investment has delivered

below-expected returns prodding the investor to cut his/her loss by

surrendering the policy and investing the amount elsewhere.

Traditionally in India, life insurance has always been looked

open as an investment product. It is for this reason, despite financial

planners recommending term life insurance plans, they have not become popular.

To support this mindset, ULIPs were launched to satisfy the

investor needs of owning an insurance-cum-investment product. Unfortunately,

the fact of the matter is that ULIPs are poor performers due to high costs and

inherent under performance.

Costs and

Performance

Being an integrated plan, a ULIP NAV combines

insurance and investment. A part of the premium paid by the policy holder goes

towards the insurance cover, while the balance is utilized for investments. As

far as the latter is concerned, the money is pooled together and invested in

various in equity and debt instruments in varying proportions, just the way it

is done for mutual funds. The policy holder has the option of selecting the

type of fund (pure debt or equity, or a blend of both).

This NAV is the value based on which the net rate of returns

on ULIPs are determined. The NAV depends on the investments made and the market

condition; in other words, the fund’s performance.

Being a market related instrument, the state of the market

has a big impact on the performance of the fund. However, research suggests

that not all ULIPs have performed well and have given reasonable returns to the

investors.

Though the market is the primary reason for ULIP’s

performance, it also depends on what fees are levied. The common costs are

premium allocation charge, top-up allocation charge, mortality charge, fund

management costs, policy administration charge, and switching costs and

surrender costs.

Besides, the surrender value is calculated as fund value

minus surrender charges (fund value = total number of units under the policy x

NAV of the chosen fund).

However, these charges differ amongst ULIPs.

Due to these costs, the residual investment of any ULIP is

not sufficient to give considerable return even if the market is doing well.

What should

you do?

Avoid it

If you have never invested in ULIPs, don’t.

If you already have, take a close look at your current

investment. Based on the criteria below, you may choose to surrender or not.

Costs

Some ULIPs have variable charges, high initially and then

lower. In case your ULIP is one and it has been years since you invested and

the maturity date is not too far off, stay invested.

If your ULIP has got ongoing regular charges which will eat

your premium and fund value, then you could surrender the policy.

Surrender charges

It could be that the surrender charges are too high if you

surrender the policy right away. If you wait for some more time, they would

come down. Once the surrender charges get low or are nil, then go ahead.

If there is no surrender charge, or it is low, then you can

go ahead.

Performance

If your ULIP is performing well post expenses, then there is

no need to exit. If your ULIP is not performing well compared to similar

investments such as mutual funds, then you could consider surrendering.

Also look at other financial instruments such as Gold ETFs,

PPF and bank fixed deposits to see whether they are giving higher returns

compared to what your ULIP has given. If yes, then maybe it is time to cut your

loss and get out.

Other

If your health condition has deteriorated after taking the

policy, it is best not to surrender. If you opt for a fresh life cover, the

company may decline the policy based on the recently developed health issues.

[Source: http://bestulipinsurancepolicy.tumblr.com/post/144187168589/should-you-stick-to-your-ulip-or-surrender-it]

Unit Linked Insurance Plan (ULIP) - An Introduction

Unit Linked Insurance Plans (ULIPs) are a category of

goal-based financial solutions that offer dual benefits of protection and

Investment. Your Unit linked Insurance Plan is linked to the capital market and

offers you flexibility to invest your units in equity or debt funds depending

upon your risk appetite. ULIPs are typically bought for long term capital gains

and offer a protection cover too.

Though much has been written about ULIPs in the past, a lot has

also changed for better. In 2010 the IRDAI issued new guidelines for ULIPs in

order to improve the returns for investors by reducing charges and to ensure

that the new product is sold and bought as a long-term protection and savings

tool. For last few years the demand for traditional insurance plans has

considerably gone up overshadowing the ULIPs. Let me bring back the focus on

what a new ULIP is all about and what’s in it for you as a customer.

What makes

ULIP a better investment product?

Avoid everyday hassle of managing stocks: Invest in ULIP

which provides you

Expert fund management

Multiple fund options – You can choose the type of fund in

which premiums will be invested.

Different Investment strategies like opportunist and balanced

approach

Adapt your portfolio,

don’t toggle it: ULIPs allow you to shift your money from one fund to

another without disturbing your long term financial plan

Fund Switching: Shift your

funds from equity funds to debt funds or vice-versa

Premium Redirection: Re-direct your future premiums to any

fund of your choice while keeping your existing fund composition intact.

Partial

Withdrawal: ULIP

provide flexibility to its policyholders to “partially” withdraw some amount of

money from his own accumulated Fund Value before the policy tenure is over.

What are

the unique features that it offers to customers?

Investment and Insurance cover

It’s a two-in-one plan in terms of giving an individual the

twin benefits of life insurance and investment.

Multiple investment options

You can invest in multiple fund options based on your life

stage needs and risk profile.

Transparency and tax benefits

You know what is the amount you are paying for the various

benefits and you will also get tax benefits under section 80 C & 10(10D) as

per prevailing tax laws.

What should one keep in mind while investing in ULIP?

Applicable charges

Payment on premature surrender

Investment fund options

Features and benefits

Limitations and exclusions

Lapsing and its consequences

Other disclosures

Busting the myths

ULIPs are

expensive: In

simple words, overall charges cannot exceed the prescribed limit set by the

regulator -the net reduction in yield cannot be more than 3% for a 10 year term

policy. This reduction in yield includes all charges except mortality and

morbidity charges. Even fund management charges (FMC) are capped at 1.35%. This

capping of charges ensures a reasonable value proposition for the customers.

ULIPS offer

low returns: There are several factors that enable the investor to get a

good return:

Invest for

long terms: ULIP offered by Life Insurance companies are the only long

term avenues for investing in disciplined manner, along with valuable life

cover.

Your choice for funds and judicious switching, redirection of

funds/premiums will ensure that the fund growth is healthy.

Source: http://bestulipinsurancepolicy.tumblr.com/post/144141727629/unit-linked-insurance-plan-ulip-an

Thursday 5 May 2016

Unit Linked Life Insurance Plans (ULIP)

In Unit linked Insurance Plan (ULIP), part of the amount paid

by the policy holder goes towards providing the insurance cover and the balance

is invested in venues of investment as desired by the policy holder. ULIP plans

are most suitable for getting life insurance coverage and also growing your

money.

Unit Linked

Life Insurance Plans:

Unit Linked Life Insurance Plans are one of the best plans if

you would like to secure a life cover as well increase your wealth at the same

time. Presenting dual benefits to the policyholders, these insurance plans

offer a life cover and assist in long term wealth creation.

These plans are way structured way to avail market linked

returns on your investments as well to get the benefits of the protection

plans. In these, a portion of premium paid by the insurer is invested in bonds

or stocks, the returns of which, are provided at the time of maturity. The

other part is used for offering a life cover to him/her.

Types of

Unit Linked Insurance Plans:

Depending on their usability and the area they cover, ULIPs

can be categorized in the following types:

ULIP for

Retirement: In retirement ULIPs, the policy-holder pays the premium

during his/her working years, for a decided period of time. This builds a

suitable amount of corpus, which, on maturity, is provided in annuities.

ULIPs for

Wealth Creation: This ULIP is primarily to increase your wealth over a

period of time. With the returns on the investment made, these plans assist

policy-holder in handling the constant inflation.

ULIPs for

Children Education: These ULIPs provide the much needed financial support

to the policy-holder, catering to the educational requirement of his/her

children. It helps in taking care of the expenses related to child’s higher

education and marriages.

ULIPs for

Health Solutions: These plans offer financial support to the

policy-holder to meet his/her medical expenses. Rising costs for addressing

health issues make it even more essential to opt for such plans.

Why ULIPs:

Transparency: ULIPs

offer a transparent format with its structures and charges clearly laid out,

allowing the insurer to make an informed decision.

Flexibility: Under

these insurance plans, policyholder can invest in differing asset classes such

as equity, money market and debt. One also has the freedom to switch between

these kinds of assets. It also offers premium flexibility.

Additional

Investment: It offers the insurer with the option to invest additional

amount, referred as ‘top-up’ at any preferred time during the tenure. This can

be done at minimal charges and guarantees various benefits.

Life

Insurance Cover: Insurer gets the freedom to select the extent of

cover he/she wants to have. In most cases, the minimum life insurance cover

that one can get is 10 times the annual premium. However, the policyholder,

depending on the policies of the company, can also get a cover of up to 100

times or even more of the annual premium.

Liquidity: One can

also partially withdraw money, which is mostly free of cost, in case of any

unpredictable event.

Tax

Benefits: ULIPs offer dual tax benefits under the sections 80C and 10

(10 D). As per current tax laws, the maturity benefits of ULIPs are tax free.

How to

choose ULIPs:

Decide your insurance objectives and then select the plan

which fulfill them

Compare: Each ULIP NAV has its

exclusive set of features and benefits. Do compare various plans online and

then opt for the one that is most suitable.

Know the varying charges such as initial charges, fund

management charges, fixed administrative charges and mortality charges, which

have been put on the product over its tenure.

Give utmost importance to your investment goals and then

consider benefits of the policy

Evaluate your risk profile and financial stability before

finalizing a certain plan. For instance, if your risk profile is high, it is

suggested to invest higher in equities.

The

required amount of Investment:

The amount of investment depends on various factors such as

the policy-holder’s risk appetite; investment goals and his/her stipulated

tenure of investment.

Things to

remember:

ULIP Charges: Be aware of the various charges which are

levied on the ULIPs. There are various sub classes in which the ULIP charges

can be categorized as Premium Allocation charges, Policy Administrative

charges, Surrender charges, Mortality charges, Fund Management charges, Fund

Switching charge and the Discontinuance charges.

Source: http://bestulipinsurancepolicy.tumblr.com/post/143888679804/unit-linked-life-insurance-plans-ulip

Tuesday 3 May 2016

Highest NAV guarantee plans likely to make an exit from the market

As per Insurance Regulatory and Development Authority (IRDA)

Unit-Linked Insurance Plan (ULIP) offered by life insurers which promises that

customer will get guaranteed highest Net Asset Value (NAV) return that the

policy has achieved during the tenure of the policy have caused confusion among

the customers hence it should be discontinued.

It is different from other highest NAV guaranteed plans as it

guarantees only 80% of the NAV take for instance if the NAV of the plan rises

to Rs 20 from Rs 10 than only Rs 16 is guaranteed.

As per IRDA product is leading to miscommunication as

customers believes that return will be high as it guarantees highest NAV return

but return are even low than pure equity fund. But insurers say that returns

are not poor but are based on market conditions.

Highest NAV guaranteed schemes guarantees returns based on

highest NAV that the policy has achieved during the term of the policy. This

product is a close ended scheme sold by companies for limited period from 3-6

months. This product has lock-in period of 7-10 years.

Highest ULIP NAV guarantee

plans typically invest its fund in debt and equities; as and in order to

protect the guarantee in the case of falling equity market insurers move funds

from equities to debt. Hence it eventually becomes a debt product and customers

are not able to get benefit of the rising equity market.

Source: http://bestulipinsurancepolicy.tumblr.com/post/143781602239/highest-nav-guarantee-plans-likely-to-make-an-exit

Monday 2 May 2016

What Are the Different Types Of ULIPs

Types of

ULIPs

Depending on

the purpose of investment ULIPS can be divided into the following types:

ULIPs for

Retirement Planning: These plans accumulate a portion of your savings over a

period of time and the corpus amount is made available to the policyholder at

maturity for purchasing an immediate annuity plan.

ULIPs for

Child Education: These plans aim at providing financial support for expenses

related to children like education, marriage etc.

ULIPs for

Wealth Creation: There are many ULIP’s with the objective of accumulating

wealth over time which will help the policyholder beat the rising costs by

offering return on investment.

ULIPs for

Health Solutions: Keeping in mind the rising medical expenses, these plans

allow the policyholder to claim for health related expenses of any kind. Some

plans may also fund your future health insurance charges.

Most

insurers offer a wide range of funds to suit one’s insurance and investment

objectives, risk profile and time horizons. Different funds have different risk

profiles. The potential for returns also varies from fund to fund

ULIPs v/s Mutual Funds

Let’s see

how ULIPs fare in comparison with Mutual Funds in various attributes:

1. Complexity

Mutual Funds

are easy to understand products, especially equity mutual funds. Whereas, ULIPs

are slightly complex as they are structured products. However, the recent

regulatory changes have to a great extent decreased the ambiguity from these

products and hence they are easier to understand now.

2. Cover Amount (Sum Assured)

Mutual funds

do not have any life cover built into them so there is no concept of life cover

(sum assured) out here. Life cover is the money paid to the policyholder’s

family if he/she dies. In ULIPs, on death, either the higher of the cover

amount or the fund value of the ULIP is paid out, or both the fund value and

cover amount is paid out – this depends on what type of ULIP you have.

3. Costs

There are no

entry loads in a MF. In fact, this is one of the biggest differences between

ULIPs and mutual funds. The only charge that investors incur is a recurring

charge on the NAV that a MF is subjected to depending on its type and corpus.

Compare that with ULIPs, there are many charges, some of which get deducted

from the premium and others from the fund value. This is precisely why ULIPs

are considered expensive in the beginning as most of the charges hit you in the

initial few years. This is also the reasons why it is advised to stick to ULIPs

for a longer term, preferably for a minimum of 10 years before you begin to see

some good returns.

Mutual funds

are cheaper, but only in the short run. Over a long period ULIPs may give you a

better return over Mutual funds as the fund management charges are lower than

mutual funds.

4. Lock-in Period

Lock-in

period is the minimum period for which an investor needs to stay invested in a

fund/plan without attracting any penalty on complete withdrawal (i.e.

surrender). When you invest in ULIPs, your money is locked in for 5 years, so

this directly affects your ability to surrender or pull out the money in case

of an emergency; however, ULIPs give you flexibility to partially withdraw from

the fund as and when needed.

In mutual

funds, there is no lock-in except when you buy tax saving mutual funds also

called Equity Linked Saving Schemes (ELSS). These get locked in for 3 years so

money is not available to you should you need it. But in all the other types of

MFs, you can withdraw your money after a year without any penalty. However in

the case of ULIPs the idea is to get life cover along with the returns and

hence the question of withdrawing before 5 years ideally should not arise.

Even though

Mutual Funds offer a lot of simplicity and flexibility in terms of investment

options and withdrawal, they simply cannot provide the risk covering capabilities

of a ULIP. For long term investors ULIP can be the best

available investment avenue. However it is the investor who needs to choose

what is best for him depending on his/her financial goals.

The

investment space is filled with options and you should look at them, identify

your financial needs and then choose the right product.

Source:

http://bestulipinsurancepolicy.tumblr.com/post/143732141304/what-are-the-different-types-of-ulips

Subscribe to:

Posts (Atom)